[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading text=”Market Commentary Update & the Banking System” use_theme_fonts=”yes”][vc_column_text]

This is Bob Barber of Christian Financial Advisors®. Yesterday morning all our advisors met to discuss the markets and what is happening in the present banking system. I asked one of our advisors, Don VandeVanter, to write a commentary on this matter. Don is a CPA and has over 20 years of experience as a Banking CFO of a large lending institution, including leadership during the financial crisis of 2007-2008. Click here to learn more about Don.

As always, feel free to reach out to Don or any of our advisors with any concerns or questions you may have by text or phone at 830-609-6986

[/vc_column_text][vc_column_text css=”.vc_custom_1678804562761{margin-top: 30px !important;}”]

What is happening with the Banks?

By Don VandeVanter, CPA

Written on March 13th, 2023

On Friday, March 10, 2023, the California Department of Financial Protection and Innovation closed Silicon Valley Bank (SVB), and the Federal Deposit Insurance Corporation (FDIC) was appointed its receiver. With over $200 billion in total assets, SVB is the second-largest bank ever to go into receivership. Signature Bank of New York (SBNY) also went into receivership yesterday, March 12.

The Federal Reserve, Department of the Treasury, and the FDIC made a joint announcement yesterday evening that they “are taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system. This step will ensure that the U.S. banking system continues to perform its vital roles of protecting deposits and providing access to credit to households and businesses in a manner that promotes strong and sustainable economic growth.” The Federal Reserve also announced it will “make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors.” The Federal Reserve has coined this program the “Bank Term Funding Program.” The full transcript can be read here:

https://www.federalreserve.gov/newsevents/pressreleases/monetary20230312b.htm.

The FDIC has assured all depositors to SVB will have full access to their money beginning today, March 13, including those deposits in excess of $250,000.

Despite these steps, most financial institutions are seeing their stock valuations decline, some of them very significantly over the last week. The losses at SVB and SBNY were not driven by bad lending decisions but rather by bad asset management. Over the course of 2020 and 2021, as the Federal Reserve and the US government poured trillions of dollars into the financial system, banks were flooded with deposits. In return for the oversupply of money, banks did not have to pay much interest at all for those deposits, with savings rates of less than 0.10 percent and 1 year CD rates of less than 1 percent. As the Federal Reserve began its fight against inflation in March of 2022, Treasury rates began to increase substantially. Investors saw an opportunity to earn some yield on their money and began withdrawing their deposits at banks to invest in Treasuries and other securities that had yields in ranges of 2 to 4 percent. Banks, such as SVB and SBNY, did not have the cash reserves to meet the demand for deposit withdrawals, so they had to begin liquidating their investment portfolios (many of which were securities bought in 2020 and 2021 with low yields) and incurred significant losses (because of the rise in interest rates). SVB disclosed last week losses on the sale of securities in excess of $1.8 billion. More information on the demise of SVB can be found here:

https://www.cnbc.com/2023/03/10/silicon-valley-bank-blowup-highlights-deposit-risks-vs-treasurys.html.

Bank analysts see the potential for more runs on banks in the short term but many believe that these banks should have time to raise cash levels to meet these demands. “The question is for depositors with balances over $250K, how comfortable are they with their bank and do they attempt to diversify?,” said Citi analyst Keith Horowitz. “We believe regionals with less diversified and large uninsured deposit bases are at risk of deposit flight but not at the speed of SVB and they should have time to tap wholesale funding markets (such as FHLB) and raise cash levels,” he added, referring to the Federal Home Loan Bank system. This is where the Bank Term Funding Program announced by the Federal Reserve should help these banks raise cash without booking losses.

At Christian Financial Advisors®, we have reviewed the portfolio of Certificate of Deposits we have purchased recently for our clients. We do not have more than $250,000 invested on behalf of any one of our clients in one financial institution but have these investments spread over many financial institutions. We would encourage any of our clients with cash holdings greater than $250,000 at any one financial institution to review the financial reports of that institution to see if they have any significant exposure in their marketable securities that may hinder them from being able to meet any demand on their deposits.

On a bright note, the recent sell-off in stocks, coupled with the news that the average hourly earning rate increase came in much lower than expected, has led to a significant increase in the value of short-term marketable securities, which may in itself help some of the banks alleviate their exposure in this area. Many are now speculating that the Federal Reserve may slow the increase in rates as well. In addition, the federal government, including President Biden, is making announcements that the US banking system is safe.

https://www.nbcnews.com/politics/politics-news/biden-deliver-remarks-silicon-valley-bank-shutdown-rcna74622

Written by:

Don VandeVanter, CPA

Approved by:

Bob Barber, Founder

Shawn Peters, Vice President[/vc_column_text][vc_empty_space][vc_column_text][/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

Market Commentary: 2022 Recap and 2023 Forward

By Bob Barber and Shawn Peters

As we begin 2023, we look back on 2022 and look forward to this new year. Last year was volatile for the stock markets as they entered into a Bear Market (a 20% decline from previous highs) in June. Today as I write this, we are squarely right in the middle of a Bear market that could last another 6-7 months based on average Bear markets lasting 13 months.

What caused this present Bear market?

This present Bear market decline is mostly from speculation that higher interest rates brought on by the Federal Reserve could cause a severe recession which so far has not happened. December increased this speculation fear, with the federal reserve raising interest rates another 50 basis points or ½%. The Fed is doing this to lower inflation and to normalize interest rates after the artificial lows during the COVID shutdown to stimulate the economy. We’re all paying the price with massive inflation caused by the Fed’s artificial stimulus and government stimulus checks.

Interest Rates

One year ago, the Fed funds rate was at zero percent. Today, the rate is 4.5% higher than a year ago. The market consensus is that the Fed will only raise interest rates another ½ to ¾ percent more, topping the Fed rate at 5 to 5.25% in mid-2023, then either stopping rate hikes or even pivoting by lowering rates.

Mathematically the first 4.5% of interest rate increases dropped the overall stock markets by approximately 20-25% or an average of 2.2% for every ½ percent the Fed raised rates. With just ½ to ¾ percent left to go, the markets should drop at most another 2-5%, based on mathematics. If it does drop more than this, it’s an overreaction and creates buying opportunities. Think of the Fed’s interest rate increases in miles. If you had a 500-525 mile trip to drive and were at 450 miles already, you are very close to your destination. This is the case for the Fed.

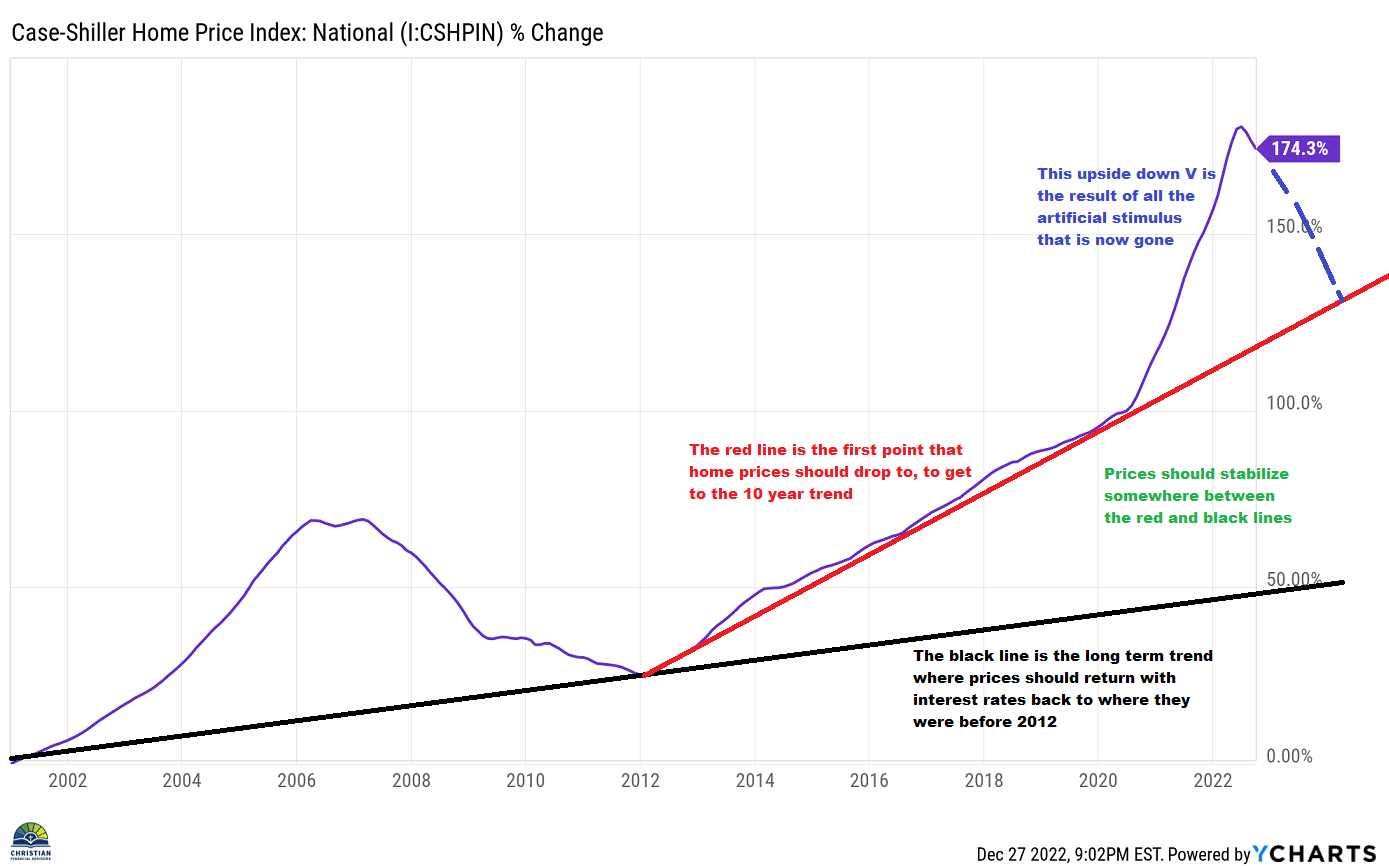

Real Estate

The area that interest rates have affected the most and will continue to affect the most is real estate. A year ago, a $3,000 monthly mortgage payment could finance a $750,000 home. That same payment will now only finance a $450,000 home at today’s rates. A $2,000 payment a year ago could finance a $450,000 home; today, it’s $300,000. From a mathematical perspective, if interest rates stay where they are, then today’s home prices need to fall enough to equalize the payment. Yes, you’re reading this correctly. That $750,000 home a year ago needs to drop to $450,000 to equalize the same payment as a year ago. A $450,000 home a year ago needs to drop to $300,000. It’s just math, and like my dad used to say, figures don’t lie. If you’re looking to buy a home today, please wait! wait! wait! I have repeatedly said that home prices were artificially high since late 2021, and now it’s proving right. It’s just math! Please review the chart I have included below.

Recovery and History

Taking all the above in consideration, we will most likely see another six months of pain in the stock market, but nothing like the first six months of 2022 when over 90% of the drop occurred. As I said above, with just 50 to 75 basis points or ½ to ¾ percent of interest rate increases left, the markets should drop no more than another 2-5% based on mathematics. Then I believe we are in for an L-shaped, possibly U-shaped recovery in the second half of 2023. All our portfolios are positioned well for the current market conditions.

We made some good buys in 2022 with the cash we took out of stocks in October of 2021 when the markets were at all-time highs and still have considerable cash left to buy more which we are doing in small increments when the markets overreact.

2022 was the worst year for the stock markets since 2008, but it was not worse than 2008. Markets rally after bear markets. For example, in the two years following the 2008 downturn, the S&P 500 rallied 39.23%, and the Nasdaq (QQQ) rallied 83.12%. Will history repeat itself? Maybe, maybe not, but it’s worth considering.

With very little left for the markets to drop now, in my opinion, I feel it is a good time to invest any cash on the sidelines by dollar cost averaging cash into the markets over the next several months before the markets possibly start to recover. When the markets get any indication that the Fed is done raising rates (or is considering pivoting to lower rates), the recovery could be so quick that any cash not invested will miss out on “the sale” that stocks are having now. The time to buy stocks is when they are “on sale,” but for some reason, stocks are the one thing people like to buy high and sell low. You should do just the opposite: buy low and sell high.

Looking Forward

Inflation should stabilize in 2023 as things continue to return to normal. In 2020, 2021, and 2022 we dealt with Covid, the Ukrainian war (which still continues), the cascading effect of supply chain disruptions, a new car shortage for lack of computer chips, etc., like we had not seen in 40-50 years. All of this is returning to normal, which is a very good thing.

In the Bible, Ecclesiastes 3:1-8 tells us there is a time for everything; war, peace, prosperity, famine, etc. This scripture assures me that the bad and good times are always temporary, so enjoy the good when they are here and rest assured that in the bad times, the good times will return.

God is in control, and we must trust Him regardless of circumstances.

If you have any questions or comments, we would love to hear from you. As always, we can be reached by phone or text at 830-609-6986 during regular business hours. You can also email us (click here) or set up an appointment (click here).

We also invite you to watch and subscribe to our weekly YouTube videos (CLICK HERE) or listen and subscribe to our weekly Podcast (CLICK HERE) on Christian Financial Topics.

Happy New Year from Christian Financial Advisors®.

Bob Barber – CEO and President

Shawn Peters- CCO and Vice President[/vc_column_text][vc_empty_space][vc_column_text][/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

By Jenna Peters

‘Tis the season to be giving…especially now that it is the end of the year and some of you are wanting to hit that tax quota for giving and donations. Did you know that donating directly to non-profits is super important for more than just the reasons you think?

I’m actually the president of a non profit organization here in our city. It’s called the New Braunfels Community Cat Coalition (NBCCC) where we provide free spay/neuters and vaccinations to local, feral cats. Our non-profit, like many out there, is 80-90% run on money from grants. Grants are a type of financial aid that donors have contributed to, and they don’t have to be paid back. Grants are amazing, and without them, we would cease to function.

However, many grants have stipulations with exactly how they can be used. For example, for NBCCC, many of our grants can only go directly to surgical supplies like gauze, suture material, vaccinations, etc, but we have so many other expenditures outside of that. Granted, surgeries and their accessories are most of our cost, but we also have repairs to the surgical clinic like new flooring. We also have marketing costs, buying t-shirts and gifts for large donors, as well as new machinery like an autoclave (a machine that sterilizes surgical instruments). All of these little things add up!

Without the extra funding that comes directly from donors, we wouldn’t be able to function nearly as well, and this is just with the non profit that I personally work with. I imagine that other non profit organizations have the same conundrum. This is why it is so important to donate to individual organizations directly so that they can use this extra funding in a way that their grants may not support.

Not only is it great for the non profit organizations, but there are also benefits to you! In general, you can deduct up to 60% of your adjusted gross income via charitable donations, but you may be limited to 20%, 30%, or 50% depending on the type of contribution and the organization (contributions to certain private foundations, veterans organizations, fraternal societies, and cemetery organizations come with a lower limit, for instance).

For specific details, just search for IRS Publication 526. Since you’re going to end up with a similar amount either way, why not help your favorite charities instead of giving more to the government? Charities use donated funds MUCH more efficiently than the government ever has and are MUCH more transparent with how the funds are used, so it’s a win-win![/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row top=”20px” bottom=”20px”][vc_column][vc_column_text]

CHECK OUT THESE OTHER AREAS OF OUR NEWSLETTER

[/vc_column_text][vc_empty_space][ess_grid alias=”grid-3″][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

By Garrett Underwood

My name is Garrett Underwood, and I have been with Christian Financial Advisors® for 7 months now as a Client Service Associate. I have had the pleasure of meeting clients and getting to serve them. I schedule meetings, handle paperwork, and help Teresa with the behind the scenes functions that keep Christian Financial Advisors® on track. In addition to being a Client Service Associate, I am the video editor for Christian Financial Perspectives. It’s a very good and informational podcast hosted by Bob Barber and Shawn Peters. It offers viewers the chance to have access to loads of financial information and helps answer a lot of common questions people might have. Especially when the markets are down and emotions start to rise, Christian Financial Perspectives can help viewers stay confident in their investments and not make drastic decisions.

Outside of working with Christian Financial Advisors®, I am married to my wife Rachel, and we have been married for 4 months now. We got to visit Playa Mujeres, Mexico for our Honeymoon, and we got to enjoy the beautiful beaches they have there. Rachel and I are both Youth Leaders for middle school at our church, Epic Life New Braunfels. We have been leaders since October of 2020, and it has been a very rewarding experience to lead the middle schoolers in their walks with Christ. We have the opportunity to not only teach the middle schoolers about Jesus, but walk alongside them as they continue to learn more about their relationship with Him. We get to pray over them, play games with them, eat pizza with them, and do worship with them. Sometimes it can be like trying to herd a bunch of squirrels that drank too much caffeine, but in the end we always have fruitful conversation and have fun together![/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row top=”20px” bottom=”20px”][vc_column][vc_column_text]

CHECK OUT THESE OTHER AREAS OF OUR NEWSLETTER

[/vc_column_text][vc_empty_space][ess_grid alias=”grid-3″][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

By Shawn Peters and Bob Barber

It has happened to the best of us. We have a big financial decision, and we jump the gun to make a large purchase before we ask for advice or really think things through, leaving us financially vulnerable afterward. Since making big financial decisions is something that we all face eventually, we’ve put together 7 recommended steps you should take before making a large purchase.

These steps can be used for anything, such as buying a new car, your first house, or even new appliances. Gaining advice and insight through using these seven steps can help take away the stress and fear of the unknown when it comes to your finances. Knowing you have the monetary means to confidently make a large purchase can offer an indescribable feeling of financial freedom.

1. Pray About It

James 1:5 “If any of you lacks wisdom, you should ask God, who gives generously to all without finding fault, and it will be given to you.”

As a Christian, all major financial decisions are spiritual ones as well, especially if it is a large one or will affect our giving. Remember, we’re the manager and God is the owner.

2. Turn To God’s Word

Proverbs and Ecclesiastes are great go-to books. There are over 1500 scriptures on stewardship in the Bible. A great example is found in Luke 16:10-13

3. Be Patient

Galatians 5:22-23 “But the fruit of the Spirit is love, joy, peace, patience, kindness, goodness, faithfulness, gentleness, self-control; against such things there is no law.”

Whatever you’re purchasing, 98% of the time there’s more of it somewhere else. Don’t fall for the urgency trap of “it’s only on sale right now!” because there’s almost always other options. Ask God to give you a peace about the purchase if it’s right or to give you a check in your spirit if it isn’t.

4. Use Math – Run A Financial Analysis On The Purchase

Luke 14:28 “For which one of you, when he wants to build a tower, does not first sit down and calculate the cost to see if he has enough to complete it?”

While being patient, research the purchase to see what it might be worth in 3, 5, or 10 years. Compare that with what a similar investment would be worth in a growth or balanced portfolio so you know your potential opportunity cost. Also, look into what the ongoing cost will be on either a monthly or yearly basis.

5. Keep Emotions Out Of It

Emotions and Finances mix together like oil and water – they don’t and never should! Step back for a second to determine if this is a “need” or a “want”. A “want” is ok if you can easily afford it but not if you can’t.

6. Seek Experienced Financial Advice

Job 12:12 “Is not wisdom found among the aged? Does not long life bring understanding?”

Discuss the purchase with your spouse and be sure you’re both in agreement. Also ask an experienced Financial Advisor as well as a parent, grandparent, or older friend who are financially successful if they believe it’s a good financial decision in the long run.

6. Apply Live, Give, Owe, Grow

There are only four ways money can be spent: for living (Live), giving to charity (Give), debt payments or taxes (Owe), or investments/savings (Grow). When one category goes up, one or two of the others will be affected. Money has to come from somewhere.

CAUTION: Many small purchases can equal one large purchase!

- Too many small purchases can quickly add up to the same as one large purchase

- This is an easy trap to fall into but can be avoided by keeping and STICKING to a monthly budget

You can make big financial decisions confidently as long as they are done with:

- Wisdom

- Insight

- Without affecting present or future giving

- Without affecting present or future savings

- A really good understanding of all costs involved

[/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row top=”20px” bottom=”20px”][vc_column][vc_column_text]

CHECK OUT THESE OTHER AREAS OF OUR NEWSLETTER

[/vc_column_text][vc_empty_space][ess_grid alias=”grid-3″][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

By Bob Barber

Christian Financial Advisors® is proud to sponsor 12 Compassion International kids – one representing each month of the year. Each monthly donation is given in our clients’ names as a representation of a birthday gift. Funds that were previously allocated to buy client birthday gifts are now donated to bless the children located in Southwest Mexico.

This year for the first time, instead of Client Christmas appreciation gifts, we also decided to use those funds and make a large Christmas donation to all the kids Christian Financial Advisors® sponsors with Compassion, so their families can have a wonderful Christmas they may not be able to have otherwise.

Compassion is a Christ-centered, church-driven, and child-focused ministry, making them distinct from other child sponsorship organizations. Their mission is to release children from poverty in Jesus’ name using a holistic approach to child development, carefully blending physical, social, economic, and spiritual care. Jesus is the core of their ministry and His life, teachings, and character shape their programs, reflect the spiritual commitments of their staff, and guide how they love people, respect communities, and cooperate with nations.

This summer, Bob and Rachael visited Compassion’s headquarters in Colorado Springs to get a first-hand look at how the ministry operates.

Next time you are visiting the Christian Financial Advisors® headquarters, please visit our Compassion wall that has all the pictures of the kids we sponsor and their stories.[/vc_column_text][vc_empty_space][vc_gallery type=”image_grid” images=”14763,14764,14765,14766,14767,14768,14769″ img_size=”medium”][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row top=”20px” bottom=”20px”][vc_column][vc_column_text]

CHECK OUT THESE OTHER AREAS OF OUR NEWSLETTER

[/vc_column_text][vc_empty_space][ess_grid alias=”grid-3″][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

By Bob Barber

As we come to the end of the year, I reflect on Christian Financial Perspectives and the many audio podcasts we have made over the last few years and YouTube videos to go with it since June 7th of this year. We now have 133 episodes at the time of this writing and growing weekly. The sweet uplifting comments from listeners and viewers on a daily basis of how much they love the program is much appreciated.

When I wanted to add video to the podcast a few years ago, I soon learned the hard way that it was not as easy as it looked. To do it right, we needed a state-of-the-art recording studio that was sound proof, high quality microphones, special lighting for videoing, a custom made professional grade backdrop, three different high-quality digital cameras for recording at different angles, high quality graphic computers, and software to record and edit. I also soon found out that an average 20-minute video would have a combined effort of 40-50 hours hours behind each one before it could go live. There is the writing of the script, editing, filming and audio, more editing, uploading, etc. before it all goes live on YouTube. It takes the talents of many people to get to the finished product you see. A big thank you goes out to all the team in helping to make this happen weekly. I know it is not easy.

As the year comes to an end, I am already putting together outlines and scripts for the first few months of 2023. Each time I write a new episode it is like drawing a new piece of art on a blank canvas. Sometimes I find myself going days, or even weeks, without creativity, and then all of the sudden it turns on like a light and I come up with many new ideas. I have really come to respect artists and writers that must come up with new content on a consistent basis for any program.

If you have not taken the time to listen to any of the 133 podcast episodes, or watch the videos on YouTube since June 7th of this year, I would invite you to watch or listen to some of them. They are all very informative and educational with a lot of thought and content behind them that I believe people want to see and hear. On YouTube, the internet, or any of the podcast platforms just search for “Christian Financial Perspectives” and you should find it easily![/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row top=”20px” bottom=”20px”][vc_column][vc_column_text]

CHECK OUT THESE OTHER AREAS OF OUR NEWSLETTER

[/vc_column_text][vc_empty_space][ess_grid alias=”grid-3″][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

By Austin Read

Have you ever wondered what waiting ten years to begin investing would do to your retirement portfolio? Let’s look at two examples: Jack and Jill. Jack, who is 20 years old, begins investing by putting an initial deposit of $2,500 into his account, and then sets up recurring contributions of $350 per month. Assuming Jack’s investments receive an average annual rate of return of 8%, and he invests this money for 40 years, his ending balance at the age of 60 could equal $1,142,9121. On the other hand, Jill, who is 30 years old, begins investing by putting an initial deposit of $2,500 into her account, and then sets up recurring contributions of $350 per month. Keeping the annual rate of return the same, by the time Jill turns 60, she could have $501,208.

With Jill waiting to start investing for retirement ten years later than Jack, she is left with almost half as much money. In fact, for Jill to reach close to the same amount of money as Jack has in retirement, and still start ten years later, she would have to double her monthly contributions to $700. What if she waited twenty years to start investing? Well, she can still reach that $1.1 million retirement goal, but now she will have to invest almost 5x as much each month for a total of $2,025. All this being said, it is never too late to start investing. As we can see, Jill still was able to reach her goals by increasing her monthly contributions. However, the main point of this article is to show that it is never too early to start investing. In fact, starting early is one of the easiest ways to set yourself up for financial freedom.

1Numbers compounded annually.[/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row top=”20px” bottom=”20px”][vc_column][vc_column_text]

CHECK OUT THESE OTHER AREAS OF OUR NEWSLETTER

[/vc_column_text][vc_empty_space][ess_grid alias=”grid-3″][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

By Don VandeVanter

Here are some common comments heard from investors lately:

“I’m waiting for the election results.”

“When will the bear market be over?”

“I’m waiting for inflation to get turned around.”

Trying to predict the timing of change in financial markets is a lot like trying to predict the weather. Unfortunately, the results are generally not even as good. Here is some wisdom from God’s Word:

“He who observes the wind will not sow, and he who regards the clouds will not reap. As you do not know the way the spirit comes to the bones in the womb of a woman with child, so you do not know the work of God who makes everything. In the morning, sow your seed, and at evening withhold not your hand, for you do not know which will prosper, this or that, or whether both alike will be good.” Ecclesiastes 11:4-6

God’s wisdom is eternal. We easily recognize that without planting a seed, it will not produce fruit. God does not give the seed to lay around idly. If the farmer waits and worries about the weather and never gets the seed planted in the Spring, there will be no crops to harvest in the Fall. The farmer will not always know when God will provide the rain or the sun to make the crops grow. The farmer’s job is simply to plant the seed and harvest the crop when God provides.

Just as God has given the seed for the farmer, He blesses us with resources and talents to be productive for His kingdom. Jesus condemns the foolish servant who hid his talent in the ground in the parable of the talents recorded in Matthew 25: 14-30, but he blesses the faithful servants who put their talents to work and produced more talents.

Many are letting the seasons of the financial markets worry them to the point of doing nothing with the resources that God has given them. Many individual investors are sitting on cash waiting for “the right time” to invest. In an article by Max Adams published by the Business Insider on October 19, 2022, he states, “There’s a massive amount of cash on the sidelines right now as markets suffer through extreme bouts of volatility and investors remain skittish.” Just as we don’t understand “the work of God who makes everything,” we don’t understand when He will provide the rain or just the right amount of sunshine to make our crops grow. We generally know that if we plant our crops in the Spring, we will reap a harvest in the fall. Sometimes, the crop will be average, sometimes it will be a bust, and sometimes it will be tremendous. The product is determined by God, we are just called to be faithful to plant and harvest.

God calls us to be productive with what He has entrusted us. With our financial resources, that means we can be generous by sharing it with others, or we can invest it to grow more and more, but we shouldn’t let it be idle. For long-term investors, we know the stock markets have produced an average gain of 10% per year since 1980, and bond markets have yielded approximately 5% per year. However, it is rare the market returns are near the average. In the last 40 years, there have been stock market gains of 15% or more in 16 years, and losses in nine of those years. So, volatility is as common as the weather is unpredictable. This year has been the worst bear market since 2008, when the market declined approximately 49% between January 1 and November 20. However, from that day forward, the market increased 20% for the rest of the year. The following year, in 2009, the total return of the S&P 500 was an amazing 23.45%. Even though it took until 2013 for the market to return to the pre-bear market levels, those that were driven out of the market at the climax of the bear run potentially missed out on returns more than 40% over the next 14 months. One interesting fact to know is that, over the last 40 years, the sum of the highest one-day gains in the stock market for each of those years makes up approximately 38% of the total gains for those 40 years.

So, if an investor is fretting about the volatility, and is not invested on the one day of the largest gain for the year, his returns are drastically affected. You never know when God is going to provide the rain. On November 10, 2022, the S&P 500 was up 5.5% for the day. Was that the end of the 2022 bear market? Only time will tell. However, there were a lot of folks sitting on cash that missed the rain God provided.[/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row top=”20px” bottom=”20px”][vc_column][vc_column_text]

CHECK OUT THESE OTHER AREAS OF OUR NEWSLETTER

[/vc_column_text][vc_empty_space][ess_grid alias=”grid-3″][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

By Bob Barber

Between Thanksgiving and Christmas, US retail sales reached $889 billion in 2021 and are expected to reach $942 billion in 2022. The top-end estimate for 2022 is $960 billion. Comparing that with 2012 numbers of $567 billion, we’re up over 66% in just ten years. That’s a LOT of Christmas shopping!

To break this down a little further, think about this for the 2022 Holiday season:

- US Households will spend an average of $7,250 during the holidays (Statista.com)

- Holiday shopping accounts for 30% of annual retail sales (MuchNeeded, 2021)

- December 15th to 24th accounts for 40% of ALL Christmas sales (MuchNeeded, 2021)

- 56% of all shoppers buy gift cards (MuchNeeded, 2021)

- The top five items people plan to buy for themselves are alcoholic and nonalcoholic beverages (33%), food – including meal prep kits (30%), clothing (30%), shoes (23%), and books (17%) (Deloitte, 2020)

The Stress of Christmas Shopping

Almost three-quarters of Americans report that money and work are significant sources of stress in their lives, according to the American Psychological Association (APA) 2007 Stress in America survey. The holidays compound the pressure, as revealed in APA’s 2006 poll on holiday stress.

Middle-income Americans are particularly affected as everyday financial pressures are amplified by demands to spend more. With the pressure to create the perfect holiday–a memorable meal, expensive gifts, elaborate decorations, and more–not having enough money to do it all causes stress to more than 60% of those surveyed on holiday stress. The worries continue when the credit card bills arrive a month later.

The Real Meaning of Christmas is about…

- The immaculate conception and virgin birth of God’s one and only son

- Unconditional love for all of us, no matter where we are in life

- Worship of THE King of all Kings – The wise men and shepherds on that glorious night

- God’s holy angels rejoicing and announcing Jesus’ birth to the shepherds

- Purity and holiness

- Humbly being born in a manger around stinky animals so Jesus could relate to everyone regardless of their economic status

- Love, joy, peace, patience, kindness, and gentleness all in one

- Gives meaning and purpose to this life

- Father, Son, and Holy Spirit

- A free offer to life here on earth filled with a purpose, meaning, and eternal life with the maker of our universe simply by acknowledging and accepting his one and only son, Jesus Christ, as your own personal Lord and Savior

The lights, the snow, the tree, the food and cookies, and the Christmas movies are all good, BUT the real meaning of Christmas is God coming to live amongst us through the immaculate conception of a virgin birth conceived by the Holy Spirit.

Isaiah 7:14 “Therefore the Lord Himself will give you a sign. Behold, the virgin shall conceive and bear a son, and shall call His name Immanuel.”

John 3:16 “For God so loved the world, that He gave His only Son, that whoever believes in Him should not perish but have eternal life.”

John 14:6 “Jesus said to him, ‘I am the way and the truth and the life. No one comes to the Father excet through me.’”

Merry Christmas from all of us at Christian Financial Advisors®!

[/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row top=”20px” bottom=”20px”][vc_column][vc_column_text]

CHECK OUT THESE OTHER AREAS OF OUR NEWSLETTER

[/vc_column_text][vc_empty_space][ess_grid alias=”grid-3″][/vc_column][/vc_row]